When you are starting business or growing successful one and moving forward, you may need to buy new equipment, upgrade technology, expand your workspace, hire more employees or increase your inventory. All these expansion plans require additional funds. In many cases, available savings may not be enough to support these big investments; this is where business loans become helpful. But if not properly, loan repayments can put pressure on your monthly cash flow, high EMIs can reduce working capital and create stress.

That is why managing business loans carefully is important. One simple but powerful tool that can help you is EMI calculator. Before taking any loan, calculating your EMI gives you clarity. Let’s understand how EMI calculator helps in business loans.

Why business loan is not always bad

Many people have negative image of loan, believing that loan is always risky or harmful. But in business world loan can be powerful growth tool when used correctly. In fact, many large and successful companies use loans strategically at different stages of their journey to expand operations, enter new markets and improve their services.

Business loan becomes helpful when:

- The loan helps increase revenue

- The return on investment is higher than interest cost

- Monthly repayments are affordable

- Cash flow remains steady and predictable

- Funds are used for productive purposes, not unnecessary expenses

For example, imagine you take loan to buy advanced machinery. This new equipment increases your production speed and improves product quality. Which help you attract more customers and increase sales and extra income generated from higher sales can cover your EMI.

Business loan becomes dangerous when:

- Loans are taken without proper planning

- The borrowed amount is higher than needed

- Repayment capacity is not calculated

- Revenue projections are unrealistic

- Cash flow is unstable

The real problem is not loan, it is poor financial planning. If business does not check how much EMI it can afford each month, even small loan can create stress. That is why smart business owners always calculate their EMI before getting loan.

Understanding cash flow in simple words

Cash flow is movement of money in and out of your business. It shows how much actual cash you have available to run daily operations.

Money coming in includes

- Sales revenue

- Customer payments

- Advance payments

- Investments from owners or partners

- Loan disbursements

Money going out includes:

- Salaries and wages

- Office or shop rent

- Raw materials and inventory purchases

- Utility bills like electricity and internet

- Marketing expenses

- Supplier payments

- Taxes

- Loan EMIs

If more money is coming in than going out, your cash flow is positive. If more money is going out than coming in, your cash flow becomes negative. For example, you may have made ₹5,00,000 in sales this month. But if customers will pay after 60 days, money is not yet in your bank account. On paper you made profit but in reality you may not have enough cash to pay salaries or EMIs.

This situation is called cash crunch, which will slow down operations. That is why EMI planning is very important before expansion. When you calculate your EMI in advance, you can check if your business can handle repayment even in low-income months.

What is EMI

EMI is Equated Monthly Installment, which is fixed monthly payment that borrower makes to lender specific date each month

Each EMI includes:

- Principal amount (loan amount you borrowed)

- Interest amount (cost of borrowing)

Your EMI depends on three major factors and if any of these change, your EMI changes :

- Loan amount

- Interest rate

- Loan tenure

How EMI impacts business stability

When you take loan, EMI becomes fixed monthly commitment. This means you must pay it whether your sales are high or low. For example, if your business earns ₹5,00,000 every month and your regular expenses like salaries, rent, raw materials and utilities add up to ₹3,50,000. This leaves you with surplus (Surplus means having more of something like money, goods, or resources than what is actually needed or used.) of ₹1,50,000. Now, if your monthly EMI is ₹1,20,000, then your remaining margin is only ₹30,000. High EMI reduces flexibility. This is why businesses must calculate EMI carefully before taking loans or you may struggle to:

- Pay suppliers on time

- Offer discounts to customers

- Invest in marketing

- Manages seasonal slowdowns

Why you always use EMI calculator before taking loan

An EMI calculator helps you know your monthly repayment amount in advance. It give clear picture of your financial commitment.

Use our EMI calculator and by entering loan amount, interest rate and tenure calculator instally shows:

- Monthly EMI

- Total interest payable

- Total repayment amount

- It removes uncertainty

When you apply for a loan, lenders may explain the terms quickly. Sometimes the focus is only on approval, not affordability. An IndiaCorporates EMI calculator allows you to pause and check the actual impact on your monthly cash flow. You clearly see how much you need to pay every month and for how long.

- Helps you adjust loan amount

Maybe you planned to borrow ₹25,00,000. But after using the calculator, you realize the EMI is too high. You can reduce the loan amount and instantly see the difference. This flexibility helps you borrow only what your business can handle. - Helps you choose right tenure

The calculator helps you test both options and decide what works best for your business’s cash flow.

Shorter tenure means:

Higher EMI

Lower total interest

longer tenure means:

Lower EMI

Higher total interest

- Allows better interest rate comparison

Even a small difference in interest rate can change your EMI significantly. By entering different rates in the calculator you can see the exact impact.

For example:

Loan at 10% interest

Loan at 12% interest - Saves time and avoids confusion

Manual EMI calculations are complicated. Small mistakes can lead to wrong planning. Use Online EMI calculator:

- Is fast

- Is accurate

- Is easy to use

- Requires no financial expertise

How EMI calculator helps in business expansion planning

When you are planning expansion, you need to answer important questions:

- Can I afford this EMI comfortably?

- Will expansion increase revenue enough?

- How long will it take to recover investment?

- Is shorter tenure better or longer tenure?

Online EMI calculator gives you clear idea of:

- Monthly EMI amount

- Total interest payable

- Total amount you will repay

- Impact of changing loan amount

- Impact of changing interest rate

- Impact of changing loan tenure

You can easily adjust loan amount, interest rate or tenure to see different results

Example scenario

Suppose you take ₹20,00,000 loan at 10% interest:

- For 3 years, EMI will be higher, but you will pay less total interest.

- For 3 years, EMI will be lower, but total interest paid will be higher

Working capital loan vs Expansion loans

- Working capital loans

Working capital loans are designed to manage short-term operational needs. These loans help maintain smooth day-to-day functioning of business. They are commonly used for purchasing inventory or raw materials, paying salaries and wages, managing rent and utility bills, handling supplier payments and covering seasonal demand increases.

- Usually short tenure (few months to 1-3 years)

- Smaller loan amounts compared to expansion loans

- Faster approval in many cases

- Maybe in form of term loans, overdraft facilities or cash credit

- Expansion loans

Expansion loans are meant for long-term growth and asset creation. These loans are used when business wants to increase production capacity, enter new markets, open new branches, upgrade technology or purchase machinery and equipment. Expansion loans generally have longer tenures because growth projects take time to generate returns. Loan amount is usually higher and lenders may require detailed business plans, financial statements and sometimes collateral.

- Longer tenure (3-10 years or more, depending on lender)

- Higher loan amount

- Structured repayment schedule

- Often requires detailed project planning

- May require collateral

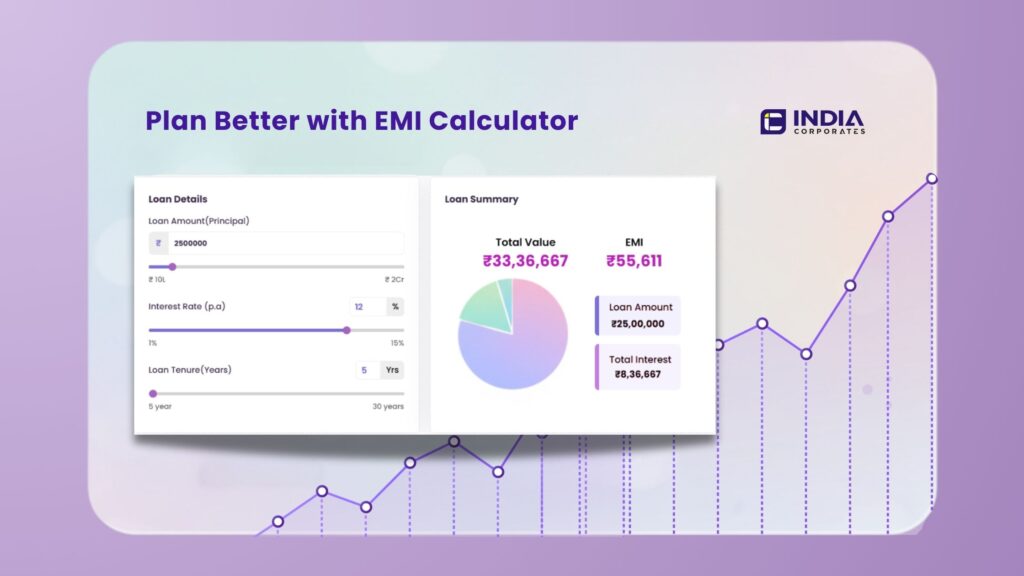

Example of EMI planning

Suppose you want to expand your manufacturing unit:

- Loan amount: ₹25,00,000

- Interest rate: 11%

- Tenure: 5 years

When you enter these values in EMI calculator, you will get

- Monthly EMI amount

- Total interest payable

- Total repayment amount

Now check your average monthly surplus. If your surplus after expenses is ₹2,00,000 and EMI is ₹55,000, it seems manageable. But if surplus is ₹60,000 and EMI is ₹55,000 risk becomes high. This simple analysis can protect your business from financial pressure.

Final thoughts: Grow smart

Business expansion is important. Growth creates new opportunities, improves brand value, increases market reach and boosts profits. It allows you to serve more customers, strengthen your position in market and stay ahead of competitors. But expansion without proper financial planning can create serious loan pressure. Taking loan is easy but managing repayment responsibly requires discipline and planning.

Before taking your next loan, take few minutes to use EMI calculator. loan is not dangerous; in fact when used correctly, it can increase growth and profitability. The real risk comes from poor planning, unrealistic projections, and ignoring repayment capacity.

No comments yet